Complete Guide to Real Estate Loans in Japan

How do I secure a property loan?

Buying real estate in Japan is expensive, but luckily debt is very affordable. If you're considering financing, there are likely a number of questions going through your mind like am I eligible for a loan? Which bank should I choose? Which loan structure is better? In this article, we will breakdown these questions and hopefully by the end of it, you will have a better understanding of the loan in Japan and can make informed decisions best suited for your needs.

If you are looking for a guide on fixed vs. floating interest rates, jump to Choosing Between Fixed vs. Floating Interest Rates in Japan: Which is better?

Table of Contents

Loan Eligibility Criteria from Japanese Financial Institutions

Lenders assess various factors to determine your eligibility for a loan such as your credit, existing debt, current income, employment, residency status, and more. The requirements for a housing loan differ across various financial institutions, but general requirements are listed below.

Applicant's Age:

Property loans can extend up to 35 years, however, banks set maximum age limits for loan completion to manage repayment risks and you may not be eligible for the full term if you are older.

Minimum age at the time of loan application: 20 years old

Maximum age at the time of loan completion: 75-80 years old

Creditworthiness & Employment Status:

Banks evaluate the borrower's credit history and credit score to assess their ability to repay the mortgage, which is typically tied into existing debt, employment status and residency status.

Debt-to-income ratio: Banks analyze the borrower's debt-to-income ratio to ensure that the mortgage payments are manageable

Employment Stability: At least 2 to 3 years of continuous, full-time employment in Japan (with exceptions considered) with stable and verifiable source of income

Residency Status: Japanese citizenship or permanent and long-term residents with a Japanese spouse

Loan Amount:

Banks will evaluate the property meticulously and adjust eligibility, loan amount and rates based on applied risk of the investment.

Property Appraisal: Banks will conducts a thorough appraisal of the property to determine its current market value and suitability (or risk) as an investment.

Loan-to-Value Ratio (LTV): The LTV ratio, representing the loan amount as a percentage of the property's appraised value, is considered to determine the risk associated with the mortgage and establish borrowing limits.

Down Payment: Can influence loan approval and terms, with considerations such as residency status, existing debt, and income levels, especially pertinent for non-residents or those with higher debt or lower income.

Which Bank Should I Choose?

There is a wide variety of available lenders you can choose from, so shop around and compare interest rates, loan terms, and fees from multiple lenders. Don't settle for the first lender you come across. Another important aspect of this step is maintaining persistence, especially if one financial institution rejects your loan application. Approach multiple financial institutions simultaneously to maximize your chances of securing the terms best for you, and balance loan terms versus compatibility.

There are 3 pools of property lenders you can generally choose from which are Mega-Banks & Trust-Banks, Regional Banks and Online Bank. Each offers various advantages and disadvantages which are weighed on risk and reward.

Mega-banks & Trust Banks

For example: Mitsubishi UFJ, Mizuho, SMBC

(+) Pro: Minimal bank default risk, On-site support, Foreigner-friendly (dependent on bank)

(-) Con: Least competitive rates, Higher hurdle for loan approval

Regional banks

For example: Bank of Yokohama, Shizuoka Bank

(+) Pro: More competitive rates than the mega-banks

(-) Con: Less competitive rates than online banks, On-site support in Tokyo is sparce

Online banks

For example: Sony Bank, SBI

(+) Pro: Most competitive rates

(-) Con: No on-site support (all conducted online)

Mortgage Structures for Individual Loans

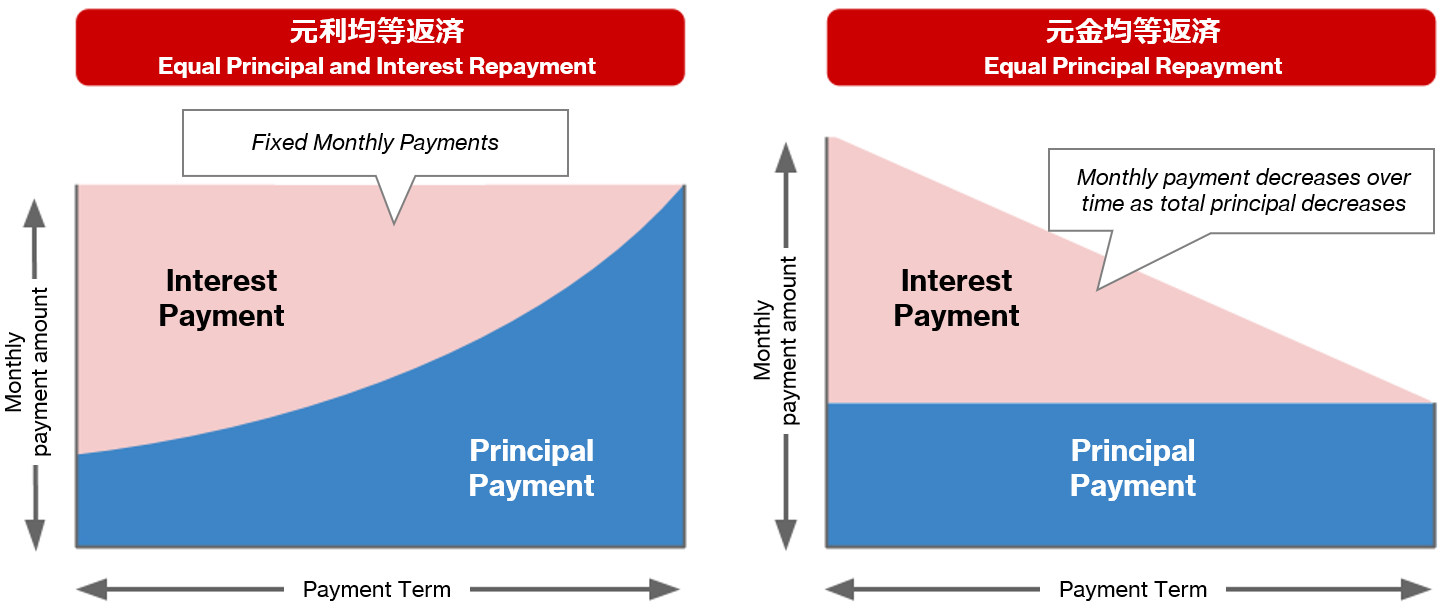

There are two primary structures in loan repayment for individual (non-corporate) borrowers: 元利均等返済 (Genri Kintou Hensai) and 元金均等返済 (Genkin Kintou Hensai). The difference lies in the way repayments are structured in Japanese loan systems:

Repayment Structures of Two Loan

Equal Principal and Interest Repayment - 元利均等返済 (Genri Kintou Hensai)

Equal payment over the course of the loan term, with the principal payment increasing over time and interest proportionately decreasing.

Over the course of the loan term, the total amount paid each period remains constant, but the proportion allocated to principal and interest changes.

Initially, a higher percentage goes towards interest, and as the loan progresses, more goes towards principal.

Equal Principal Repayment - 元金均等返済 (Genkin Kintou Hensai)

Decreasing payment structure over the loan term with higher initial payment

Equal payments for principal amount borrowed over the loan term with interest payments decreasing over time as outstanding principal balance decreases with each payment.

Initially, a higher monthly payback compared to Equal Principal and Interest Payment, but as the loan progresses, monthly payments will be lower.

Recommendation

Ultimately, the choice between these repayment structures depends on individual financial circumstances, risk tolerance, and the length of your hold period. However, we recommend that you select the Equal Principal Payment as real estate is a long-term investment and your total payment amount is lower, your financial burden decreases over time and your money goes towards paying down your principal rather than interest.

On the other hand, for investment property owners utilizing the Equal Principal and Interest Payment structure, the interest portion can be treated as an expense, enhancing the tax-saving effect in the initial stages of investment. It is advisable for borrowers to thoroughly assess their situation and, if possible, seek advice from financial professionals before making a decision.

The typical merits and demerits associated with the two loan structures can be summarized as follows: